Trendlines: What explains the surge in sales of mini excavators in North America?

12 June 2023

Mini excavators have seen their popularity surge in North America. What has changed? Chris Sleight, managing director of Off-Highway Rsearch, explains.

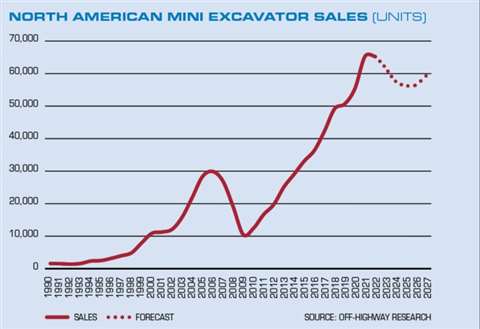

In the 1990s, a good year for the mini excavator market was around 4000 machines sold across the whole of North America. That’s a tiny number if you consider that skid-steer loader sales were running at around 50,000 machines per year for most of that decade and there were also 25,000-30,000 backhoe loaders going into the market each year.

Things started to change in the 2000s, when mini excavator demand moved rapidly to the 10,000 and 20,000 unit per year mark before peaking just shy of 30,000 machines sold in 2006. After that, the decline in housebuilding in the wake of the sub-prime crisis and then the global recession both took their toll for the next decade.

But when the mini excavator market bounced back, it did so with a vengeance. In 2015, sales topped 30,000 units for the first time and for the next six years a new sales record was set. The number of machines sold was particularly striking in 2021 and 2022, with 65,000 mini excavators sold in each of those years.

Fundamental change

The surge of the last two years was directly related to the boom in residential building during the pandemic, and compact track loaders also enjoyed a similar spike for similar reasons. However, the long-term growth trend points to something more fundamental taking place.

As these machines have sold in greater and greater numbers, loader backhoe sales have declined. Sales have been less than 10,000 units per year for the last three years and, tellingly, there was not much of a rebound in 2021. The same trend has been seen in Europe over the last 10 to 15 years, with mini excavators gaining greater and greater acceptance while the traditional product (in certain markets, the backhoe loader) has steadily lost ground.

“Big” minis preferred

But whereas in Europe the market is focused on smaller machines of 2.5 tonnes or less, which relates to the maximum gross vehicle weight allowed on a standard driving license, demand in North America only really begins at 2 tonnes. Machines from 2 to 6 tonnes (the upper cut-off of Off-Highway Research’s mini excavator classification) account for around 85% of sales.

Chris Sleight, managing director, Off-Highway Research.

Chris Sleight, managing director, Off-Highway Research.

This preference for relatively big mini excavators is one of the key reasons why the segment is forecast to remain strong over the next five years. These machines are large enough to have applications in infrastructure construction as well as smaller scale residential work.

This also extends up into the smaller classes of crawler excavators, which have again been a huge area of growth over the last 10 to 15 years. Machines in the 6 to 12 metric tonne size class now represent around 35% of all crawler excavator sales. Compare this to 15 to 20 years ago, when the most popular class was 20 tonne crawler excavators, and the market tended in general toward much heavier machines.

Clearly, tastes and preferences change over time. In the case of mini excavators, contractors have been swayed by the smaller footprint and 360-degree slewing of these machines, compared to the large footprint and more limited working arc of a loader backhoe. Plus, of course, a mini excavator would tend to be significantly cheaper to buy than a loader backhoe.

Off-Highway Research is the international market research and forecasting division of KHL Group.

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

POWER SOURCING GUIDE

The trusted reference and buyer’s guide for 83 years

The original “desktop search engine,” guiding nearly 10,000 users in more than 90 countries it is the primary reference for specifications and details on all the components that go into engine systems.

Visit Now

CONNECT WITH THE TEAM